PRELIMINARY PROXY STATEMENT

SUBJECT TO COMPLETION, DATED JANUARY 31, 2020

LEISURE ACQUISITION CORP.

250 West 57th Street, Suite 2223

New York, NY 10107

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON , 2020

TO THE STOCKHOLDERS OF LEISURE ACQUISITION CORP.:

NOTICE IS HEREBY GIVEN that a special meeting of stockholders of Leisure Acquisition Corp. (“LACQ”), a Delaware corporation, will be held at a.m. eastern time, on , 2020, at the offices of Proskauer Rose LLP, counsel to LACQ, at Eleven Times Square, New York, New York 10036. You are cordially invited to attend the special meeting, which will be held for the following purposes:

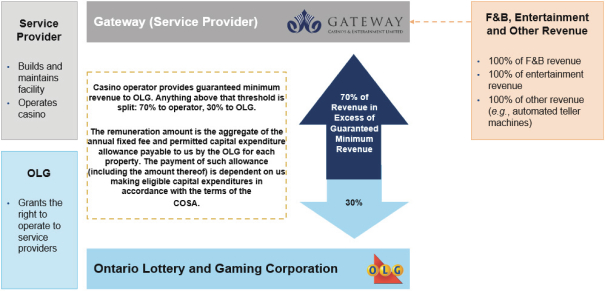

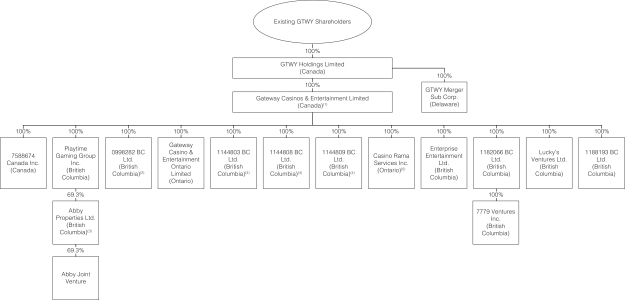

| (1) | to consider and vote upon a proposal to approve the business combination described in this proxy statement/prospectus, including the Agreement and Plan of Merger, dated as of December 27, 2019 (the “Merger Agreement”), by and among LACQ, GTWY Holdings Limited, a Canadian corporation (“Holdings”) and the holding company for Gateway Casinos & Entertainment Limited (“GCEL”), and GTWY Merger Sub Corp., a Delaware corporation and a wholly owned subsidiary of Holdings (“Merger Sub”), which, among other things, provides for Merger Sub to be merged with and into LACQ with LACQ being the surviving company and becoming a wholly owned subsidiary of Holdings (the “Merger”); and the other transactions contemplated by the Merger Agreement, including adoption of the amended and restated articles of incorporation of Holdings, (together with the Merger, the “Transactions”) and the related agreements described in this proxy statement/prospectus—we refer to this proposal as the “business combination proposal”; and |

| (2) | to consider and vote upon a proposal to adjourn the special meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies if LACQ is unable to consummate the business combination contemplated by the Merger Agreement—we refer to this proposal as the “adjournment proposal.” |

These items of business are described in the attached proxy statement/prospectus, which we encourage you to read in its entirety before voting. Only holders of record of LACQ common stock (“LACQ Shares”) at the close of business on , 2020 are entitled to notice of the special meeting and to vote and have their votes counted at the special meeting and any adjournments or postponements of the special meeting.

After careful consideration, LACQ’s board of directors (the “LACQ Board”) has determined that the business combination proposal and the adjournment proposal are fair to and in the best interests of LACQ and its stockholders and unanimously recommends that you vote or give instruction to vote “FOR” the business combination proposal and “FOR” the adjournment proposal, if presented.

Consummation of the Transactions is conditional on approval of the business combination proposal at the special meeting. The adjournment proposal is not conditioned on the approval of any other proposal set forth in this proxy statement/prospectus.

All LACQ stockholders are cordially invited to attend the special meeting in person. To ensure your representation at the special meeting, however, you are urged to complete, sign, date and return the enclosed proxy card as soon as possible. If you are a stockholder of record of LACQ Shares, you may also cast your vote in person at the special meeting. If your shares are held in an account at a brokerage firm or bank, you must