Disclaimer (cont’d)

FORWARD-LOOKING

INFORMATION

This Presentation contains “forward-looking information” within the meaning of applicable securities laws in Canada and the United States.

Forward-looking statements may relate to Gateway’s, LACQ’s, or the combined company’s future financial outlook and anticipated events or results and may include information regarding our financial position, business strategy, growth

strategies, growth objectives, budgets, operations, financial results, taxes, dividend policy, regulatory developments, plans and objectives. All statements other than statements of historical fact are forward-looking statements. The use of any of

the words “anticipate”, “plan”, “contemplate”, “continue”, “estimate”, “expect”, “intend”, “propose”, “might”, “may”, “will”,

“shall”, “project”, “should”, “could”, “would”, “believe”, “predict”, “forecast”, “pursue”, “potential” and “capable” and similar

expressions are intended to identify forward looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such

forward-looking statements. In addition, this Presentation may contain forward-looking statements attributed to third party industry sources, the accuracy of which has not been verified by LACQ or Gateway. No assurance can be given that these

expectations will prove to be correct and such forward-looking statements included in this Presentation should not be unduly relied upon. Statements containing forward-looking information are not historical facts but instead represent

management’s expectations, estimates and projections regarding future events or circumstances. Forward-looking information contained in this Presentation and other forward-looking information are based on our opinions, estimates and assumptions

in light of our experience and perception of historical trends, current conditions and expected future developments, as well as other factors that we currently believe are appropriate and reasonable in the circumstances. Despite a careful process to

prepare and review the forward-looking information, there can be no assurance that the underlying opinions, estimates and assumptions will prove to be correct.

Additionally, any estimates and projections contained herein have been prepared by the management of the Company and involve significant elements of subjective

judgment and analysis, which may or may not be correct. This Presentation includes certain estimates, targets and projections that reflect Gateway management’s assumptions concerning anticipated future performance of Gateway as provided to LACQ

on December 19, 2019. Such estimates, targets and projections from are based on significant assumptions and subjective judgments concerning anticipated results, which are inherently subject to risks, variability and contingencies, many of which

are beyond Gateway’s control. These assumptions and judgments may or may not prove to be correct and there can be no assurance that any projected results are attainable or will be realized. LACQ, Gateway, any third-party source providing

information and each of their respective representatives disclaims any and all liability for any loss or damage (whether foreseeable or not) suffered or incurred by any person or entity as a result of anything contained or omitted from this

Presentation (including information from third-party sources) and such liability is expressly disclaimed.

You are cautioned not to place undue reliance on any forward-looking statements, which speak only as of the date of this Presentation. The forward-looking information contained in this Presentation represents our expectations as of the date of this Presentation or the

date indicated, regardless of the time of delivery of the Presentation and is subject to change after such date. However, we disclaim any intention or obligation or undertaking to update or revise any forward-looking information whether as a result

of new information, future events or otherwise, except as required by law.

All of the forward-looking information contained in this Presentation is expressly

qualified by the foregoing cautionary statements.

NON-IFRS MEASURES

This Presentation makes reference to certain financial and other measures commonly used by financial analysts in evaluating the financial performance of companies and by the

Company’s management in evaluating its operations, including companies in the gaming industry that are not presented in accordance with international financial reporting standards (“IFRS”). These measures are not recognized measures

under IFRS and do not have a standardized meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other companies. Rather, these measures are provided as additional information to complement those IFRS

measures by providing further understanding of our results of operations from management’s perspective. Accordingly, these measures should not be considered in isolation nor as a substitute for analysis of our financial information reported

under IFRS.

We use non-IFRS measures including “Adjusted EBITDA”, “Adjusted EBITDA Margin”,

“Adjusted Property EBITDA”, “Adjusted Property EBITDA Margin”, “EBITDA”, “Free Cash Flow”, “Free Cash Flow Conversion”, and “Pro Forma Adjusted EBITDA” and these measures should not be

considered as an alternative to net income (loss), earnings per share or any other performance measures derived in accordance with IFRS as measures of operating performance, operating cash flows or as measures of liquidity. For further details on

these non-IFRS measures including relevant definitions and reconciliations, see the “Financial Overview” section of this Presentation.

As of September 30, 2019, Starlight Casino Edmonton and Grand Villa Casino Edmonton are considered discontinued operations in Gateway’s consolidated financial

statements. These properties are referred to in this presentation as “Non-Core Properties.” Where indicated in this presentation, financial information of Gateway excludes the Non-Core Properties.

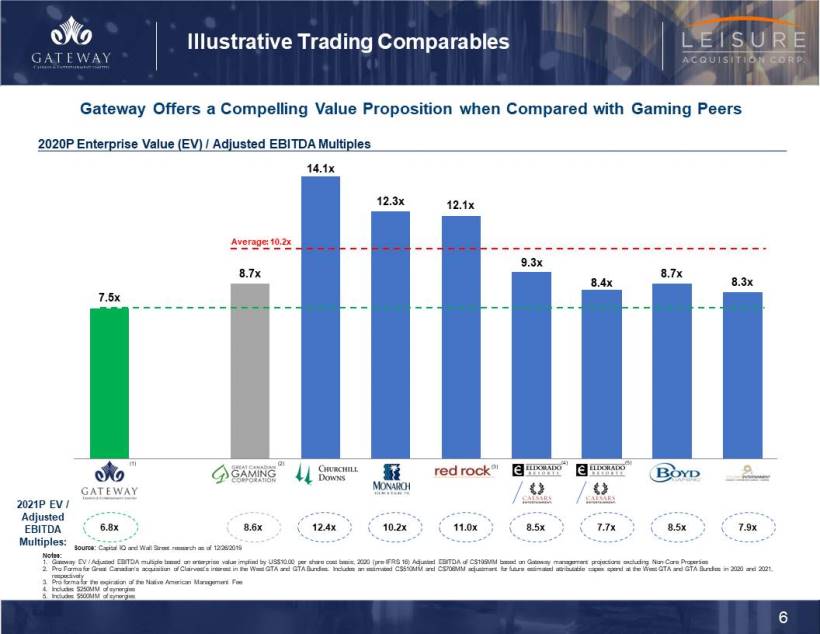

COMPARABLE COMPANIES

Certain information presented herein compares the Company to other issuers and such data sets are considered to be “comparables”. The information is a

summary of certain relevant operational attributes of certain gaming issuers and has been included to provide interested parties an overview of the performance of what are expected to be comparable issuers. These issuers are in the same industry,

provide similar services and operate in similar regulatory environments and each should be considered an appropriate basis for comparison to the Company. The information regarding the comparables was obtained from public sources, has not been

verified by LACQ, the Company, or any of their respective affiliates and if such information contains a misrepresentation, interested parties do not have a remedy under securities legislation in any province or territory of Canada. There are risks

associated with comparables, including the integrity of the underlying information and the ability to isolate specific variables which may impact one issuer and not another. There are risks associated with making investment decisions based on

comparables including whether data presented provides a complete comparison between issuers. Interested parties are cautioned that past performance is not indicative of future performance and the performance of the Company may be materially

different from the comparable issuers. Accordingly, an investment decision should not be made in reliance on the comparables.